Fuel for thought

Published over 9 years ago. See the latest and most current information on Fuel for thought.

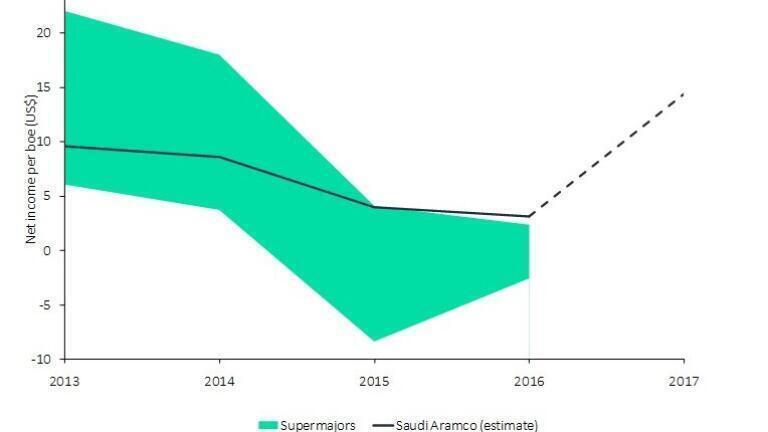

Faced with declining government revenues from the oil and gas sector after the oil price crash and looking to diversify its economy, Saudi Arabia is reportedly planning to list 5% of its state-owned oil giant, Saudi Aramco, in an Initial Public Offering (IPO) in late 2018. With a view to making the listing more attractive by improving Aramco’s cash flows, the government published a decree on March 27 slashing the company’s tax rate from 85% to 50%. However, even taking into account the effect of this change, there is significant uncertainty over whether the company can achieve a much-vaunted US$2 trillion valuation.

The 85% tax rate previously applied combined with a 20% royalty rate resulted in one of the most taxing fiscal regimes in the world, significantly depressing Aramco’s cash flows. Under this regime, the fiscal take would be over 92% of free cash flow from Aramco’s upstream operations. The tax cut reduces the fiscal take to 65%, bringing the operating environment in line with global averages. Although Aramco’s operations and finances are notoriously opaque, we estimate that this will increase Aramco’s annual net income over the coming five years by over 230%. In recent years the counter-effects of a high tax burden and low cost base are estimated to have resulted in a net income per barrel of oil equivalent similar to the levels achieved by other major oil companies, but Aramco’s performance will be significantly boosted by the tax cut.

This boost to net income per barrel (bbl) translates into a significant increase in the Net Present Value (NPV) of Aramco’s upstream portfolio, which represents the core of the company’s operations; Aramco has exclusive rights to produce oil in Saudi Arabia, OPEC’s largest producer. However, the final valuation of these assets is highly sensitive to the sustainability of current production levels, which is highly uncertain given the secrecy surrounding their operations. The base case envisages the onset of mild production declines in the middle of the next decade, resulting in a valuation of US$601 billion; US$405 billion of this value is the result of the tax cut. However, Saudi Aramco’s latest reported oil reserves, for the end of 2015, are 261 billion barrels. Such reserves could allow the company to maintain current production for over 50 years before the onset of declines, yielding a significantly higher valuation of US$815 billion. These valuations assume a flat oil price of approximately US$55/bbl, but in a high case where prices escalate by 2.5% from 2019, the value of the high-reserves case exceeds US$1 billion. Conversely, there is downside risk on the valuation should prices fall again.

PIN 27.3 June/July 2026